It’s a common scenario for older Australians – asset rich, cash poor. Owning a valuable home and having little income can be an issue, but there are ways around this other than selling your house. Below we look at the workings of a reverse mortgage.

What are they?

It is called a reverse mortgage as unlike a traditional mortgage, where you borrow money at the outset and repay the loan over time, a reverse mortgage sees the loan balance actually increase with time as no repayments are made.

This gives you the opportunity to turn the equity in your own into cash. For some, a reverse mortgage is a great way to stay in your home, borrow money for living expenses and have the loan repaid when you sell or pass away.

A reverse mortgage works by allowing you to borrow a certain percentage (typically 10-20% of the value of your home). Over time, interest gets charged on the initial loan amount, and this compounds, so the final balance of the loan will be higher than the initial loan amount. When you sell your home or pass away, the loan is repaid.

The money you borrow can be taken in the following ways:

- Regular income stream e.g. a monthly payment

- Line of credit

- Lump sum

- Or any combination

A common way to utilize a reverse mortgage is to take a lump sum initially, and then have regular payments.

If interest rates sky rocket and home prices crash, it is remotely possible that the loan balance could end up being higher than the value of the home. To protect borrowers, any reverse mortgages taken out from September in 2012 have negative equity protection – essentially meaning you won’t end up owing the bank more than your home is worth.

The cost of a reverse mortgage will depend on:

- How much you borrow

- The amount you borrow

- The interest rate and fees

- How long you have the loan

While you are living in the house, you don’t need to make repayments. Some loans will give you the option of making payments on the interest portion of the loan, in order to reduce your overall cost.

Case Study

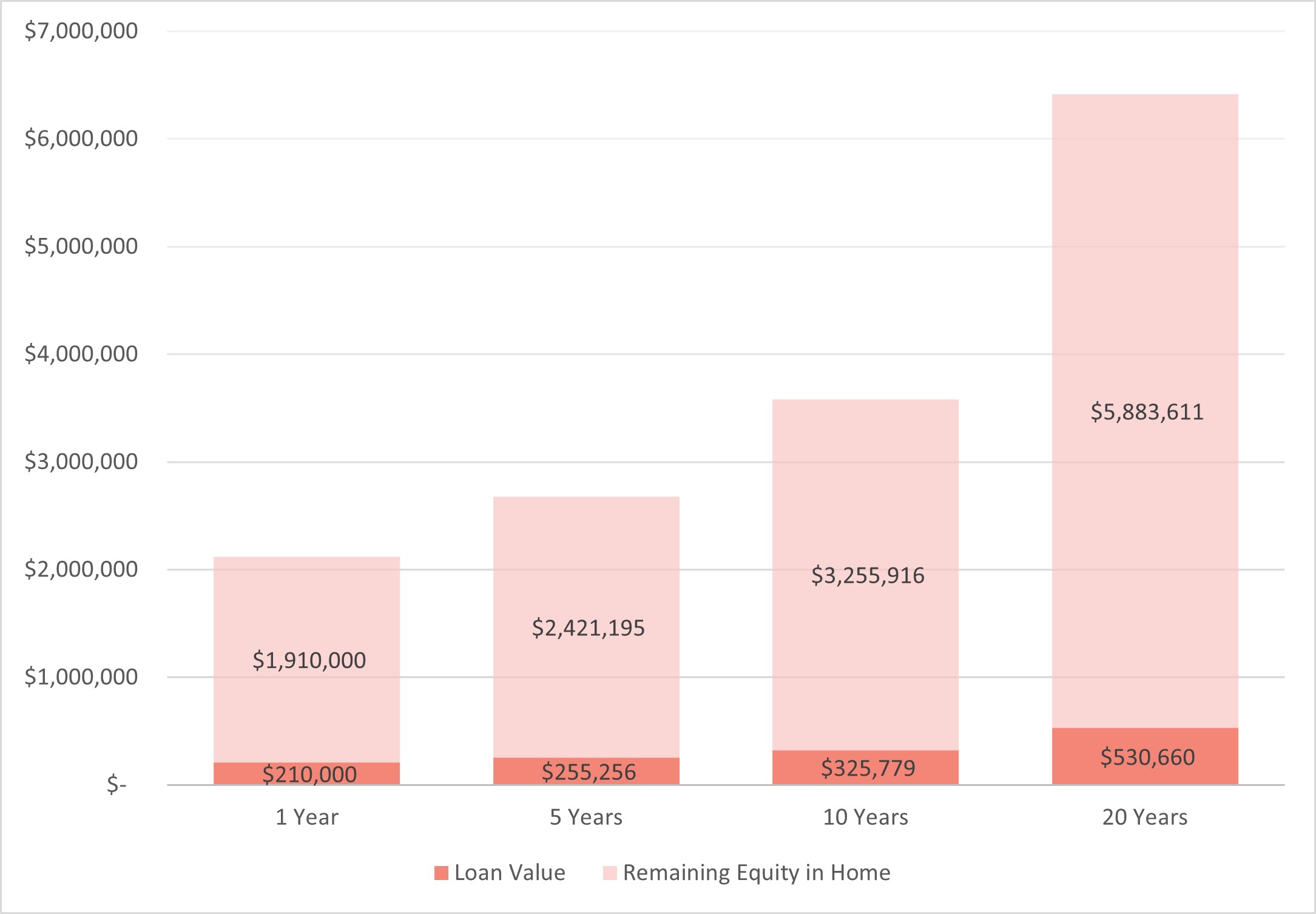

Here is a case study on a reverse mortgage and how their loan balance looks over time. John and Sally, both aged 67, own their home valued at $2,000,000. They borrow $200,000 (10% of their home value) at an interest rate of 5% pa and we assume the value of their house grows at 6% pa.

The day after they take out their reverse mortgage, they have $1,800,000 net equity in their house. Over the next 20 years, the loan grows to $530,000 while the value of their home increases to over $6,000,000 (over three times it’s original value due to the impact of compound interest).

As you can see in the table, even though the value of the loan increases (as no repayments are being made), the value of the home and the net equity also increase.

Loan and home equity over 20 years

Assumptions. Starting home value $2,000,000. $200,000 initial loan. 5% pa interest rate. 6% pa home growth. 20 year time frame.

There are a few pros and cons of reverse mortgages:

| Pros | Cons |

| You can stay in your family home as long as you would like | Interest is compounded, so the loan value will increase over time |

| Improved funding and gives you greater choice about your retirement lifestyle | Reduces the value of your estate when you die |

| Flexibility to provide income and lump sum payments | Drawing funds from your property now may reduce what you could potentially access later |

| You will remain the owner of your home, benefitting from future capital growth | Loan to Value Ratios (LVR) are generally lower compared to standard home loans; your age dictates the LVR for a reverse mortgage |

| No repayments are required until sale of your home or death, leaving more cash available for living expenses | Reverse mortgages tend to have slightly higher interest rates than regular mortgages as the loans are generally repaid at the end of the term |

| Reverse mortgages are regulated with consumer protections (including no Negative Equity) | Can impact Age Pension payments if assessed as an asset or income |

Reverse mortgages have a role to play in retirement income and are well suited in certain situations. Before applying for a reverse mortgage, always seek financial advice.

What Can Align Financial Do For You? Visit our homepage to learn more about our service. If you would like to speak to us about your financial circumstance, please feel free to give us a call on 02 9913 9995. We are located in Narrabeen on the Northern Beaches of Sydney.

.

Disclaimer: This post has been prepared for general information purposes only. It is not specific advice to any particular person. You should consult an authorised Align Financial adviser before making financial decisions. Align Financial | Financial Planner Northern Beaches | Servicing North Narrabeen, Narrabeen, Mona Vale, Elanora Heights, Newport, Avalon, Palm Beach | Enquire with us online

.